Time to Review Your Retirement Strategy

PROPOSED DIVISION 296 TAX

TIME TO REVIEW YOUR RETIREMENT STRATEGY

While the Division 296 Tax (Div 296 tax) legislation is yet to be passed by Parliament (Superannuation (Building a Stronger and Fairer Super System) Imposition Bill 2026), we are certain to see some form of tax imposed on ‘large’ superannuation balances.

Thankfully, version 2.0 of Div 296 tax is simpler and fairer than the first iteration.

Once the tax has been introduced, those with ‘large’ super balances (> $10m) may find superannuation a less attractive vehicle to predominantly hold their wealth. Modelling of the cost of the new tax indicates a modest tax impost closer to $3m, but this increases significantly when the $10m threshold is exceeded.

Where possible, a member who has met a condition of release may choose to reduce their Div 296 tax by keeping their total superannuation balance (TSB) below $3m each year. While possible, this may not be an attractive option for some clients where they have other sources of income and their balance is not much greater than $3m – the tax on the amounts withdrawn and held outside the fund may exceed the Div 296 tax liability.

For some members with ‘large’ superannuation balances, where they have met a condition of release, they may prefer to withdraw part of their superannuation balance and invest through another structure, such as a company or trust, which will avoid the ‘death benefits tax’ (generally 15% on the taxable portion of the member balance received by the Deceased Estate) where payments are made to an Estate on the death of a member. Control of these structures can be passed on via the member’s Will.

Every superannuation member will need to review their superannuation interests and made decisions to suit their personal circumstances – there is no single ‘correct’ decision or course of action that may be applied.

This article is specifically focused on self managed superannuation fund (SMSF) member balances and does not consider defined benefit interests.

GENERAL OVERVIEW

The commencement date for the new tax is proposed as 1 July 2026.

Div 296 tax is levied on the individual (it is a personal tax liability) and can be paid by the individual or the member can lodge a release authority to enable the tax to be paid by the fund.

All of an individual’s superannuation interests will be aggregated to determine their total superannuation balance, and whether they exceed the $3m or $10m thresholds at the beginning or end of the year (in the transitional year, only the end of year balance will be applicable).

Thresholds are indexed in line with CPI as follows:

- $3m threshold increased in $150k increments

- $10m threshold increased in $500k increments

Earnings from the following funds are excluded:

- Foreign superannuation funds.

- Constitutionally protected funds, and funds related to judges;

- Non complying superannuation funds.

Note, while the earnings on these funds are excluded for Div 296 tax, the balances will be taken into account in determining the member’s TSB (where more than one superannuation interest is held).

Exemptions from the proposed Div 296 tax include:

- Structured settlements (personal injury); and

- child death benefit payments.

Key Terms for the calculation of Div 296 tax:

- Superannuation Earnings

- Total Superannuation Balance (of all superannuation interests)

- Proportion of earnings subject to Div 296 tax

HOW IS DIV 296 TAX CALCULATED?

Step 1 – Member’s Total Super Balance (TSB)

There is a new ‘universal’ definition of TSB, which is the sum of each of the individual superannuation interest plus interests that support a death benefit income stream (includes reversionary pensions).

Where the member balance at 30 June 2027 is less than $3m, Div 296 tax will not apply to the 2027 year.

Where either the opening or closing TSB is more than $3m from 1 July 2027, the Div 296 tax calculation will be applied.

Step 2 - Calculate the Div 296 tax earnings

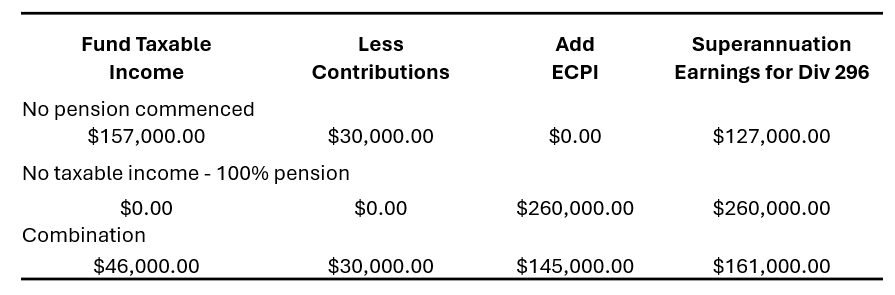

The Div 296 tax earnings calculation is based on the fund’s taxable income, with the following adjustments:

Relevant taxable income or loss:

- is calculated in the usual way – includes franking credits and gross foreign income;

- Capital gains are offset against capital losses and net gains are further reduced where they qualify for 1/3 discount;

- Modified capital gains will be calculated where the fund has elected to ‘opt in’ to revaluing all assets for Div 296 tax purposes, and there has been a CGT event relating to one or more of these assets;

- Excess tax losses and capital losses are carried forward;

- Pre 2017 gain amounts are disregarded (for those funds with 30 June 2017 deferred notional gains).

Contributions:

- Assessable concessional contributions, as these are included in the fund’s taxable income.

Net exempt current pension income (basically assume the fund is not in ‘pension mode’):

- Add regular exempt current pension income (ECPI) less deductions that would have been attributed to the income (and excluded under ECPI);

- Net ECPI may be a negative amount.

Non arms length income (NALI):

- NALI is tax at 45%, so it is excluded from the earnings calculation.

Pooled Superannuation Trust component:

- This does not apply to SMSFs.

If overall Div 296 tax earnings are negative, the amount will be Nil for the year.

Earning calculation examples:

Where there is more than one fund member…

The fund will apportion earnings for a multi member fund (the fund may need an actuary’s certificate, as with ECPI):

Share of Div 296 tax fund earnings x time-weighted average member super interest

Total of all member superannuation interests

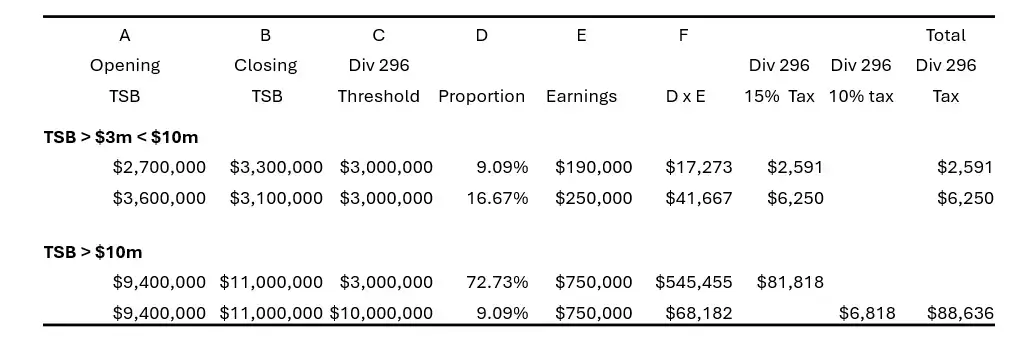

Step 3 – Determine the Taxable Proportion of Earnings

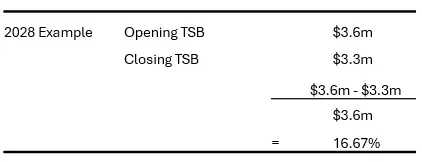

The taxable proportion/percentage is the amount of the members’ TSB that exceeds $3m or $10m, divided by the members’ TSB opening or closing TSB, whichever the greater (apart from the transition year, when you use the closing TSB).

Total Superannuation Balance Less Either $3m or $10m threshold

Total Superannuation Balance

For members with TSB in excess of $10m, two calculations are required – one at 15% and one at 10%.

Step 4 – Apply the Taxable Proportion and Calculate the Tax

Div 296 Tax Calculation Examples

PROCESS OF REPORTING AND PAYING THE TAX

- Trustees provide an annual statement to the ATO;

- The ATO will calculate Div 296 tax and issue assessments;

- Payment is required 84 days from the date the ATO issues the assessment – individuals can request release from their superannuation balance during this time;

- ATO will create a new Div 296 tax debt account and GIC/SIC will apply to late payments.

TRANSITIONAL MATTERS

- Transition year is 2026/27 – in this year only the closing member balance (30/6/2027) will be used. Trustees can sell assets and reduce a members’ TSB below $3m to avoid the tax.

- Capital Gains Tax - Cost base adjustments

- Choice to ‘opt in’ is irrevocable;

- Applies to the market value of assets DIRECTLY held at 30 June 2026;

- Choice applies to all directly held assets, regardless of whether they increase or decrease in value (loss assets will have their cost base reduced);

- Cost base adjustments relate to the SMSF – if a member exits the fund, this concession will no longer apply to their member interest;

- Only used to calculate Div 296 tax – existing cost bases continue to apply for accounting and tax (need to keep at least two records of cost bases – three if there were 2017 cost base adjustments);

- Include election to ‘opt in’ in SMSF 2027 income tax return – lodge before the due date for lodgement of the SMSF return;

- Trustees must keep records for 5 years after the CGT event.

TRUSTEE/MEMBER CHOICES

- Do Nothing

- Opt in or not? Even if fund balance is below $3m – it may grow to above the indexed $3m level;

- Sell loss assets pre 30 June 2026;

- Reduce a member’s balance to reduce the tax liability?

DEATH

Div 296 tax does not apply where a member dies during the 2026/27 year, as their member balance will be nil at the end of the year.

On death, a member may have a nil closing balance but still have an opening member balance. In 2027/28 and later years, the opening balance of the deceased member is used for calculating Div 296 tax, and the closing balance is assumed to be zero.

Reversionary pensions will increase the surviving members balance and may push the surviving spouse, who may have a superannuation balance of less than $3m, over this threshold.

The taxable percentage of the fund’s income also increases where there is only one member remaining, which increases the Div 296 tax.

The Legal Personal Representative (LPR) pays the Div 296 tax for the deceased. The LPR may need to delay the administration of the Estate to ensure the Div 296 tax has been paid prior to making a final distribution. This could significantly delay the finalisation of the Estate.

OTHER SPECIFIC CONSIDERATIONS/STRATEGIES

- Has the member met a condition of release? If so, could they reduce their member balance by withdrawing cash/assets from the fund? Is it tax effective to do this?;

- Regardless of whether a condition of release has been met, a member may consider future investing in different structures, such as a company or trust. This may also simplify Estate planning, where shares in an investment company can be left to beneficiaries of a deceased Estate (with 30% franking credits available on dividends paid to shareholders);

- The timing of the disposal of assets is critical – ideally a fund would stagger disposals, and the resulting capital gains, over a number of years to reduce the earnings in any given year;

- Illiquid Assets – these will be included in the members’ TSB, but can’t be realized immediately (or the realization costs may be prohibitive), such as farm assets, other property or unlisted assets that can’t be readily converted to cash;

- Should the trustee review asset valuations for some assets? Lower valuations result in lower Div 296 tax;

- Where a SMSF holds units in a unit trust, the taxable amount of the income distribution from the sale of assets held by the unit trust is assessable on sale, regardless of whether the cost base of the units has been adjusted;

- Where a SMSF holds units in a unit trust, does the trustee dispose of these units pre 30 June 2026? Where this is an option, should the asset be held directly by the SMSF rather than by the Unit Trust? Ensure transfer costs are factored into this consideration;

- Where a SMSF holds units in a unit trust, does the Unit Trustee sell the asset and wind the trust up in the same year, so that the loss on disposal of units offsets any distributed capital gain?;

- Earnings issues – for members joining a fund, and for those leaving, they will still receive a proportion of the fund earnings based on their opening or closing balance (if leaving due to separation, recommend using the CGT rollover relief so no automatic capital gain is triggered);

- Inheriting spouse superannuation – combining superannuation interests can take the beneficiary member over the $3m threshold – may need to review reversionary pension arrangements;

- Where Div 296 tax payments are made from the fund, please ensure they are made from the balance with the highest taxable percentage;

- Should death benefits be paid to the Estate of the deceased? You may need to review existing reversionary pensions and include an adjustment clause in the Will to ensure that any Div 296 tax is to be paid from the Estate (as it may be difficult to claw this back if final distributions have been made from the Estate);

- ‘Death benefits tax’ is to be considered in payments to the Estate – specifically where you have the ‘last member standing’, single member funds and aged members.

As you can see, the imposition of this additional tax on large superannuation balances may be simple to calculate, but the implications for members impacted by the tax will require specific advice.

Even funds where members won’t immediately be impacted (where balances don’t exceed $3m) they may need to update their retirement plans now, including consideration of the capital gains option to revalue all assets, dispose of loss assets, review reversionary pension arrangements, update their Wills etc.

Disclaimer This article is for general information only. Every effort has been made to ensure that it is accurate, however it is not intended to be a complete description of the matters described. The article has been prepared without taking into account any personal objectives, financial situation or needs. It does not contain and is not to be taken as containing any securities advice or securities recommendation. Furthermore, it is not intended that it be relied on by recipients for the purpose of making investment or superannuation decisions and is not a replacement of the requirement for individual research or professional advice. The article is purely the opinion of the author on the day and this article is record of that opinion. No part of this article should be used elsewhere without prior consent from the author.

Michelle Wilson 3 March 2026